The Big Picture

Dave’s Economic Assessment – April 2009

Index

- Executive Summary

- Undisputed Facts

- Not Quite Undisputed Facts

- The Good News

- My Opinion & Predictions

- What Must be Done

- Best Case Scenario

- Worst Case Scenario

- Most Likely Scenario

- Recommended Reading

Executive Summary

This work is the product of years of research and months in the writing. It’s an attempt to give a high-level overview of all the relevant pieces of the economic situation this country finds itself in. Most of the ideas have been gleaned from experts far more knowledgable than myself – I’m not an economist. These are simply the most important ideas and facts I’ve come across in my extensive reading about the current situation over the last nearly two years. None of these facts are a secret, nor have they come to light recently. Much of what legislators claim to be surprised about has been known for nearly two years.

For a long and somewhat technical overview, baseline scenario does a great job. I also recommend their financial crisis for beginners. This American Life did some great episodes as well. Here is the short version: We have had 30 years of steadily increasing debt – public, private, and financial sector. Everyone who remembers the depression is long dead or retired, and modern day economists have spent much of this time convincing themselves that the laws of the market, the business cycle, and recessions in general were a solved problem, never to bother us again. The arrogance coupled with the absolute corruption of our current campaign finance system has ensured that wall street has been dictating policy the entire time. Our treasury and Fed continue to pretend that this is simply a liquidity problem, and not a massive ponzi scheme founded on theft and lies. It is nothing more than legalized theft. Trillions of dollars in profit go to people taking insane risks, and when all that can be stolen has been, the bottom drops out. Insolvent banks (including foreign ones) get bailed out by the tax payers to a tune of (so far) 8.5 TRILLION dollars. This is more expensive in adjusted dollars than every expensive thing ever combined – WW1, WW2, the Marshall plan, etc. Most of the bad debt has already been transferred to the public. Fannie and Freddie bought up every piece of garbage mortgages they could get, expanding their balance sheets till they held $5T of the $11T US mortgage market. 90% of these mortgages were originated by private companies, many of them fraudulent. AIG wrote $2.7T worth of unregulated ‘insurance’ with $100B in capital. The taxpayer now owns them both.

We live in a corporatocracy – privatized profits and public losses. We will be paying for their crimes for decades. The $34T problem of the credit default swap market hasn’t even been touched, and it has the ability to do much more damage than a mere $5T in mortgages gone bad. At least mortgages are backed by something of value.

The naive belief in market fundamentalism combined with corruption on an untold scale has brought the world economy to the brink of disaster, and no one in power is even attempting to address the real problems. Our treasury and Fed continue to pretend that this is simply a liquidity problem, and not a massive ponzi scheme founded on theft and lies. The new bank rescue plan is nothing more than the same crappy plan Bush proposed in 2008, but rebranded. It gives private investors a very small risk with huge potential profits, and the losses will go to the taxpayer.

House prices will continue to decline until they are below the historical mean. The losses from the continued increase in foreclosures will require ever more bailouts for the rich bankers who caused the problem. The recession will feed on its downward momentum, only slightly slowed by any government stimulus attempt. When interest rates rise, government intervention will become impossible and there will be massive spending cuts. This will be the ‘other shoe’ that will bring the second wave of pain and create a true depression. There will be no recovery in the next year or two. The DOW will fall below 6000 inside of 2 years, with only the artificial GDP boost from the massive stimulus spending there to provide a little lift. Once that effect has worn off, the market will go back to dropping.

The only course of action I can recommend at this time is the most conservative possible. Get out of debt, live beneath your means, and save. Invest in safe bonds and hedge inflation concerns with precious metals (I see them as a safe harbor, not an investment that will do well). Individuals and businesses should be prepared to survive on a lot less for a long time. Oil and the energy crisis haven’t gone away – OPEC is cutting back production to get the price back up – I guess they didn’t hear the ‘drill baby drill’ campaign marketing slogan. Oil and oil companies might not be a bad investment, especially if China can keep growing their economy.

Undisputed Facts

- The cost of the bailouts is staggering. Estimates vary (7.5 trillion, ABC news), and we can be assured it will keep getting more expensive. Our GDP is 14T. Add another 3T for the Bush wars and in a very short time, this country has added a year’s worth of its TOTAL OUTPUT to our national debt for which we got nothing. It’s the equivalent of a person (let’s call him George) who makes 50k a year go out and put 45k on the credit card in a few years. The 2009 budget deficit is expected to reach 1.8T, mainly because the cost of the wars is no longer being hidden by dishonest accounting. No one expects the budget deficit to shrink anytime soon.

- Fannie Mae and Freddie Mac used to be quasi-private entities. They were caught using fraudulent accounting years ago, but it wasn’t punished. They funded themselves through corporate bonds which explicitly stated that they weren’t backed by the government (wink, wink). They were the king violators of leverage ratios, getting to 200:1 amid more and more requests to be allowed to take on even more. This was the dumping station for as many bad mortgages as private mortgage originators could unload. They now hold a combined $5T in mortgages, and are now owned by the government. All of the investors who knowingly invested in a private corporation have been protected, with the taxpayers paying off all their debt.

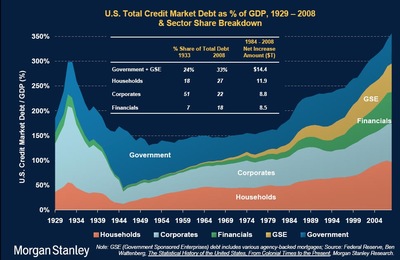

- Much of the claimed economic growth of the last 10 years has been nothing more than spending debt. This chart shows where much of that spending came from:

- The fraud that caused the economic meltdown is not being prosecuted. Homeowners and mortgage originators lied about income, ratings agencies gave AAA ratings to garbage, including giving that rating to AIG when they were levered so high, and banks are still allowed to lie about their balance sheets using level 3 assets and CDS to fill giant holes. Bernie Madoff was just one cockroach – if you see one, there are dozens more.

- Credit default swaps. This is the monster in the closet that is waiting to pounce. The estimated size of the CDS market, an over-the-counter (OTC) system that is totally unregulated, is 34 trillion. Anyone can write a CDS contract and there is no margin supervision, no requirements that parties be able to pay. JP Morgan holds $90T in derivatives contracts. AIG, which our government now owns 80% of, wrote $2.7T worth of this unregulated insurance with no more than $100B in capital. That’s a 27:1 leverage ratio, which is essentially infinite. AIG has only been bailed out to the tune of $144B (the furor over bonuses is almost exactly 1/1000th of the problem). Some of this went to foreign banks and hedge funds. There is literally trillions of dollars worth of this worthless insurance, which was fraudulent when it was written (because contract law dictates that signing a contract when you lack the means or intention of paying off is fraud). So far, we have been paying out claims on these ridiculous promises (without which btw, every major bank in the world would be massively insolvent). If we really try to cover all those losses, the cost could double the already ridiculous number. If we don’t pay these fraudulent commitments, we will suffer far worse, says the ransom note from Deutsche Bank. So far, our government has done everything it can to assure rich oligarchs that we’ll take good care of them.

- The personal savings rate in this country hit the lowest level since 1933, fueled by a decades-long credit binge. In the last quarter, it has jumped to 5%. This isn’t surprising, considering the huge hit household net worth has taken. With 70% of our GDP coming from consumer spending, we find ourselves in a bizarro world where we are actually being told we have to stop saving money to save the economy.

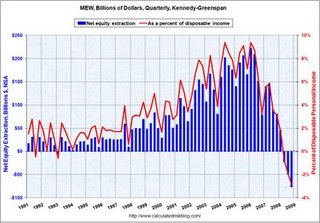

- Ponziconomy. Going back to George – if a person spends 45k on the credit card, he can’t claim that as income. If we as a nation do it, somehow that new debt counts as income. In 2008 we spent $300B on a tax rebate, and the spending from that new debt was counted as GDP. A quick look at this chart or this one:

shows pretty clearly where our ‘economic growth’ has come from in the last few decades – it’s just debt. Debt that must be paid off with interest, or defaulted. There are no other options.

shows pretty clearly where our ‘economic growth’ has come from in the last few decades – it’s just debt. Debt that must be paid off with interest, or defaulted. There are no other options. - The fed has begun buying its own treasuries, to the tune of $1T. Talk about the snake eating its own tail. This is a private bank with unlimited power to bankrupt the taxpayer. They doubled their balance sheet in 5 weeks. They traded T-bills to banks for their garbage assets, and now plan to dump those assets on the treasury (that’s us) in exchange for more T-bills. Here’s a great explanation of why the fed’s attempt to keep interest rates and spreads low will fail.

- Since 2002, wall street has donated over $1B to washington campaigns. Does anyone believe this was a gift, and not a purchase?

- Our financial sector has grown from 6% to 15% of our economy. When that much of the economy is based on complicated financial instruments that no one understands, that’s not a good position to be in. That % will no doubt shrink, with nothing to take its place.

- The treasury has announced their bank rescue plan (again), and it’s nothing more than the Bush TARP plan with some rebranding. The FDIC will ‘entice’ private investors by financing the purchases in such a way that the investors have lots to gain and very little to lose (read taxpayer subsidy). Here are two excellent explanations.

- The unfunded liabilities of medicare and social security are roughly $70T. This will not be a problem for your children, but one that gets real bad real soon.

- The US has zero reserves, while China and Japan have massive FOREX holdings. Who does that give the power to in deciding how the world economy will work? Why does Germany have ten times the gold the US does?

Not Quite Undisputed Facts

- The US is completely failing in its attempts to address the crisis. House prices haven’t slowed their decline, banks are still worth nothing in the stock market, and as we watch our national debt skyrocket, the economy only gets worse. This is simply due to the fact that our leaders are lying about nature, cause, and solution to the problem. Here is Geitner layout out the new plan:

Over the past six weeks we have put in place a series of financial initiatives, alongside the Recovery and Reinvestment Program, to help lay the financial foundation for economic recovery. We launched a broad program to stabilize the housing market by encouraging lower mortgage rates and making it easier for millions to refinance and avoid foreclosure. We established a new capital program to provide banks with a safeguard against a deeper recession. By providing confidence that banks will have a sufficient level of capital even if the outlook is worse than expected, more credit will be available to the economy at lower interest rates today — making it less likely that the more negative economy they fear will take place.

House prices stabilized? nope. Markets still declaring banks worthless in spite of the banks and the Fed saying they’re well-capitalized? yep. But this is all about the plan to save banks from their own stupidity by buying up all the garbage that the market says is worth say 30 cents on the dollar when the banks would much prefer it be worth 80 cents:

The funds established under this program will have three essential design features. First, they will use government resources in the form of capital from the Treasury, and financing from the FDIC and Federal Reserve, to mobilize capital from private investors. Second, the Public-Private Investment Program will ensure that private-sector participants share the risks alongside the taxpayer, and that the taxpayer shares in the profits from these investments. These funds will be open to investors of all types, such as pension funds, so that a broad range of Americans can participate.

Third, private-sector purchasers will establish the value of the loans and securities purchased under the program, which will protect the government from overpaying for these assets.

The new Public-Private Investment Program will initially provide financing for $500 billion with the potential to expand up to $1 trillion over time, which is a substantial share of real-estate related assets originated before the recession that are now clogging our financial system. Over time, by providing a market for these assets that does not now exist, this program will help improve asset values, increase lending capacity by banks, and reduce uncertainty about the scale of losses on bank balance sheets. The ability to sell assets to this fund will make it easier for banks to raise private capital, which will accelerate their ability to replace the capital investments provided by the Treasury.

3 paragraphs, 3 lies. First, when he says ‘share the risk’ he means ‘the taxpayer takes almost all of it’. Here’s Paul Krugman’s take:

Why was I so quick to condemn the Geithner plan? Because its not new; its just another version of an idea that keeps coming up and keeps being refuted. Its basically a thinly disguised version of the same plan Henry Paulson announced way back in September.

…Now, early on in this crisis, it was possible to argue that it was mainly a panic. But at this point, thats an indefensible position. Banks and other highly leveraged institutions collectively made a huge bet that the normal rules for house prices and sustainable levels of consumer debt no longer applied; they were wrong. Time for a Swedish solution.

Lie the second: Letting the market set prices will protect the government for paying too much for the assets (I can’t help but laugh even typing that). Here’s Karl Denninger:

Let’s say that I am a bank (“financial institution”) with $100 billion in “toxic assets”. I have them on my balance sheet at 80 cents on the dollar. The market has them marked at 30 cents. We do not know what the held-to-maturity performance will be, since that requires knowing the future, although for the moment let’s assume that they are cash-flowing at the present time.

What I (the bank) do know, however, is that if I sell them at 30 cents I take a monstrous loss – perhaps enough to force me under Tier Capital limits and thus render me subject to an FDIC enforcement action. I therefore will not sell for 30 cents so long as I have any belief whatsoever that the cash flow – or any government subsidy – will exceed that value.

If I, as a “financial institution” can participate as a bidder in these auctions I can foist off my loss onto the taxpayer. Here is how I can rig the game so as to avoid an otherwise-inevitable loss:

- I become a “bidder” and “bid” on my own assets at 75 cents.

- I am providing 5 or 10% of the money. The rest is covered by Treasury, The Fed and the FDIC via guaranteed bond issuance.

- The loan, ex my contribution, is non-recourse. That is, I can lose 5 or 10% of the total portfolio purchased, but nothing more.

Now the “assets” (a passel of CDOs?) turn out to be worthless. I lose 5% of $75 billion, or $3.75 billion that I put up, plus the other nickel on the original mark, but that’s all.

The taxpayer gets hosed for the remaining $71.25 billion dollars.

This can and will be done if the “sellers” of these assets are allowed to bid either directly or indirectly as it provides a means for banks to intentionally dump bad assets at a certain loss that is much smaller than their expected realized loss over time, shifting the rest of the loss to the taxpayer.

Lie the third: Creating a market where one doesn’t exist. There always has and always will be a market for these assets. The buyers simply don’t want to pay what banks feel they are entitled to.

To read anything the previous or current administration says, one would think there’s just a few bad loans that need to be swept up and everything will be just fine! No mention of our crippling debt, our debt-fueled unsistainable national lifestyle, not one word about having to change the ridiculous way we’ve been living. Sadly, pathetically, unforgivably, they continue the game of trying to keep the old game going, no matter how obviously impossible that wish.

- How it could all come apart: You think things are bad now? There are many scenarios out there for things to get much worse. The most likely is a jump in interest rates, which MUST eventually happen. Eventually someone will start to recover (like China) and investors will start to want more return instead of a safe haven. Here is one way the US could go broke. If Interest rates rise, the government would be forced to slash spending across the board. Here’s a handy chart you can watch yourself – if it goes up, that’s very bad.

- We’re all Keynesians now. The only economic theory left most economists think has a chance to help is the idea that government can step in and be the ‘buyer of last resort’ to make up for the massive shortfall in demand that happens with recessions. No one knows if this will work or not. Massive government spending halved the unemployment rate during the depression, but didn’t end it until WW2 created even more massive demand from outside the country. WW2 also wiped out incredible amounts of national debt for Germany, Britain and France – maybe that was what fixed things? At any rate, this country had the option of spending lots of money in the first depression because it had been fiscally responsible and had no debt at the time. We are already at the point where we can barely make the interest payments on staggering debt accumulated during the biggest economic expansion in history. The squirrel has prepared no nuts for the winter, and in fact owes Guido the squirrel more than he can ever pay. And it’s snowing.

- Free market fundamentalism aka laissez faire economics aka Reaganomics is bankrupt. A completely failed ideology that brought us to the brink of ruin. Even Alan Greenspan, Ayn Rand devotee and free market poster child, admitted his entire philosophy was deeply flawed:

“I made a mistake in presuming that the self-interests of organizations, specifically banks and others, were such as that they were best capable of protecting their own shareholders and their equity in the firms. He further called this mistake “a flaw in the model … that defines how the world works.” (emphasis mine)

Oh gee, the short-term self-interest of the richest, most powerful people on the planet might not be the best rudder to use to steer the global economy? What a shocker. Here’s a perfect example of letting the free market do everything: investment in oil development nearly perfectly tracks the price of oil. BP is shutting down solar manufacturing plants. Is this how energy policy should be made? What happened to ‘drill baby drill’? A discarded marketing ploy, and nothing more.

- The Bezzle defined:

“In many ways the effect of the crash on embezzlement was more significant than on suicide. To the economist embezzlement is the most interesting of crimes. Alone among the various forms of larceny it has a time parameter. Weeks, months, or years may elapse between the commission of the crime and its discovery. (This is a period, incidentally, when the embezzler has his gain and the man who has been embezzled, oddly enough, feels no loss. there is a net increase in psychic wealth.) At any given time there exists an inventory of undiscovered embezzlement in – or more precisely not in – the country’s business and banks. This inventory – it should be called the bezzle. It also varies in size with the business cycle.”

We are living in a bezzle bubble. The damages are still unknown and continue to be revealed. There is no way to know when we will find all the damage, nor how much it will end up being. Investors know this, and won’t return to our markets until it’s over.

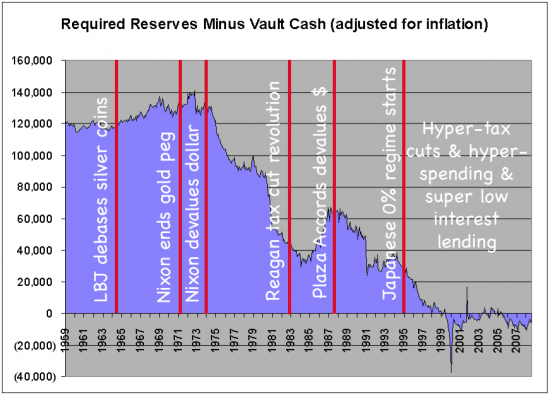

- Banks are insolvent, and are lying on their balance sheets. Our corrupt leaders have driven reserve requirements into negative territory:

Borrowing from the Federal Reserve has gone from $60B to $600B in one year. CDS and mark-to-model accounting are time bombs waiting to go off, once the banks make sure they know who will take the brunt. The market has declared these banks to be insolvent through their stock prices, in spite of our government and the banks themselves saying they are ‘well capitalized’. When the investment community thinks both are lying, that is a major crisis of confidence that has nothing to do with a recession. - Millions of Americans are screaming for justice. Calls to the congress about the bailouts are 300:1 against, and they are ignored. Millions have signed petitions for war crimes prosecutions of the Bush administration. For mortgage originators who made billions lying and breaking countless laws creating garbage loans guaranteed to default. For the ratings agencies who rated pure garbage split in fancy ways to be AAA, the best possible credit score. For banks who grossly violated the already ridiculous leverage standards in place pumping out billions in junk CDOs to municipalities, pension funds and investors, and who only got caught with a small fraction of the worthless loans they served as the conduit for. For the hundreds of thousands of wealthy individuals hiding their wealth in the queen’s offshore tax havens. The populist rage will continue to feed upon the many indignities it has suffered until it boils over into a destructive mob, unless some justice starts to be dealt.

- The financial media has been a huge part of the problem. CNBC admits they knew all about how AIG was set up to be a pass through agent for a backdoor bailout for banks like Goldman Sachs and Deutsche Bank, and they just didn’t tell anyone. A Kiplinger article from March 31st, 2009 calling the bottom in the stock market. All through the bubble, the financial press fed the flames, scaring people that they would be ”priced out of a house’ if they didn’t buy now. Same with stocks. The press used to be a proud component of our democracy, now it’s a crass and transparent wealth transfer system.

“I am… for freedom of the press, and against all violations of

the Constitution to silence by force and not by reason the

complaints or criticisms, just or unjust, of our citizens against

the conduct of their agents.” –Thomas Jefferson to Elbridge Gerry,

1799.The corporate media have proven themselves completely deficient in their duties to inform or even report basic facts. Only in the turbulent free-for-all of the Internet can a meritocracy have a chance to replace the broken, bleeding and corrupt system that plagues us today. Jon Stewart makes some good points.

- Our government has known about this problem since at least 2007 and ignored it. I spoke at a town hall with my house representative and laid it all out in October 07, almost a year before Bush decided it was his last card to play in the election shenanigans game. Not until it fit a political purpose (and the financial system was on the brink of collapse) did anything get done. And it was the worst possible action. Hundreds of billions in money handed to banks with no accountability, no restrictions on bonuses, and no idea where the money went. Complete outsiders have been writing about the coming storm for years (April 2007) – is it more comforting to think our government too stupid or too corrupt to acknowledge the problem earlier?.

- The Good News

I realize this isn’t a fun document to read. It’s not all bad news, though:

- The US has the world’s largest economy (25% of the globe), enjoys one of the highest standards of living, and has the most wealth. When bad things happen, it hurts those on the bottom the worst.

- This country has a proud history of finally doing the right thing (slavery, suffrage, banking regulations after the depression, child labor laws). If the will of the people is restored as the primary driver of our laws & government, we can overcome just about anything.

- Americans have long turned to one another for support in times of need. Tales abound on the Internet about how people took care of each other in the depression, in a time when everyone became poor at the same time.

- The Internet is the cause of, and solution to, so many of our problems. Within it lies the hope of bringing democracy and justice to the entire planet, of replacing our corporatist media machine with a distributed, incorruptible network. And it only comes at the price of possibly destroying the very systems upon which we have come to depend.

- The worst president in history is finally gone, and an adult is in charge again. One who overturned Ted Stevens’ conviction that was so badly botched by Bush’s DOJ that it set him free, obviously guilty or not. What a perfect antithesis to a man who ordered the firings of district attorneys who refused to prosecute non-cases against political enemies. Obama overturned a ridiculous ban on stem cell research, giving hope that science and facts might play a role in decision making once again.

My Opinion/Predictions

Our single biggest national security issue has nothing to do with bearded guys with guns. It is the laughably weak economic position we find ourselves in. We have traded all our manufacturing capacity (without which we never would have pulled out of the depression) for some short-term profits for corporate executives. How does a service-based economy recover when we’re too debt-laden to buy any services from each other? Our trade imbalance is on a long-term worsening trend, so what do we export? Cash. Around the world our money goes to build up rival economies, our oil money goes to support dictators and criminal regimes (like Saudi Arabia), and we bankrupt ourselves trying to police the world. Was it Bush’s ambition to follow in Russia’s footsteps in Afghanistan? It destroyed their country, yet we think we can ‘win’ something there. Never mind it’s already been 8 years and no one can say what our goal is there.

We complicate the tax code more and more every year thanks to lobbying from CPAs and their ilk, until no one can do their own tax return. We support an entire class of white collar jobs preparing tax returns when they could be doing something useful (not to mention more wasted money running the IRS). The drain that our lawyer class has on our economy makes the CPAs look like a good investment.

Our government’s budget rules are as simple as they are asinine: spend 100% of the money you’re given or your next year’s budget gets cut. Tomes could be written about the idiocy behind this, but it doesn’t even get a mention. Every department of every agency in the entire government spends 100% of its budget, every year. It doesn’t matter if the library buys new computers every December, or if schools have dozens of people cleaning a few desks each summer, because everyone does it. Know someone with a government job? Ask them and they’ll tell you their ‘spending stupid money at the end of the year’ stories.

Our politics is driven by the need to raise millions or tens of millions of dollars to run for office, so our government is bought & paid for by whoever can write those checks. In 2008, the ‘securities and investment’ sector donated $142M to campaigns. That’s less than 1% of the bonuses they paid themselves that year, in which the Dow lost 30%. Conveniently, most of the cost of a campaign goes to buying 30 second ad spots on major networks – no conflict of interest there. Our mainstream media outlets are all subsidiaries of giant multi-global corporations with their own agendas, with profit being the one and only job. As a result, public debate on any topic is dominated by the idiots who can scream the loudest, the irrelevant sideshows that will sell the most adspace, and whatever Rupert Murdock decides will benefit his corporation the most.

In this utterly absurd environment, this so-bad-you-wouldn’t-believe-it-in-a-novel society we have made of ourselves, only the toughest to implement and most inspired solutions have any chance of fixing the problem. The populist rage will not settle down without some major justice being dealt – that doesn’t look likely. Trillions of dollars of private investment capital will only step back into our markets if they are convinced it’s not a rigged game, and they can count on what companies will be worth tomorrow – so far every step by our government has been to obfuscate, to pretend, and to bail out the very worst. The only goal is prolonging the games, not addressing the fundamental flaws in this great country. This is why you constantly hear about ‘propping up house prices’ and ‘getting banks lending again’ and ‘getting consumers spending’ again. This is the language of ‘everything’s fine, just keep shopping’. We are way, way past that bullshit.

The Obama factor. Obama is one of the finest examples of democracy ever. He is the only president in modern times to be elected with 88% of his contributions coming from individuals limited to $2700 each (most less than $200). Before the primaries even started, everyone in the media was predicting an easy primary win for Clinton. Obama doesn’t owe massive corporations for funding his campaign like pretty much every other candidate in modern times. His positions on most subjects are reasonable and well-considered, and it appears he actually wants to do the right thing. At the end the day, I fear that Humpty Dumpty has been ground into the sidewalk and not much can be done to save him quickly.

The problem with Obama is the same problem with all politicians in Washington. He has no background in finance or economics, nor do almost any of our lawmakers. They are helpless without their advisors telling them what will fix our economic problems, and so they are easily manipulated by wall street. The 1999 repeal of Glass-Steagall was actually sold as more regulation, when in fact it was the equivalent of stripping the brakes & bumpers off every car in America. Obama has picked up almost exactly where Bush left off in dealing with the economic crisis: he gets tough with the auto industry, forcing them to re-negotiate their contracts while at the same time the US effectively owns AIG, Citibank, Bank of America and other banks from all the money we have doused them with, yet we are somehow powerless to stop them from using our money to do whatever they want. Until the person we voted into office has the financial chops to make his own decisions, we will never even know who is deciding the financial future of our $3.6T government. Our leaders lack the expertise to ask even the simplest questions – like how we can fix a problem caused by too much easy credit with lots more easy credit.

Some of the plans coming out of Washington give me hope, but it’s too early to tell. It’s too much to hope that reasonable and prudent regulations get passed – not while wall street is pulling the strings. There are so many burdensome regulations already, that waste countless dollars of those trying to do the right thing, meanwhile bald faced crooks like Madoff go untouched for more than 10 years. Make no mistake, the banking system must be regulated, but this was a failure of enforcement. Countless existing laws have been broken, but failed to be enforced thanks to the concerted destruction of that capacity over the last few decades. The profit making, investment & insurance side of things – where high risk and paychecks go along with regular bankruptcies – should be firewalled from the actual banks. And any corporation whose failure might endanger any part of the system should be forcibly broken up into pieces small enough that we can allow any one of them to fail. If the less adaptable didn’t die, evolution wouldn’t work. Capitalism absolutely depends on the failure of companies and people who make bad decisions.

Let’s not forget how much the American people are to blame. At the end of the day, politicians are our employees and we have been absent. Have you spent more time watching American Idol or reading about the Trillions that have been stolen from you? Have you marched, phoned, written letters or done anything to make your voice heard? How much has to be stolen from you to get some action? Protests abound in other countries, but there have been no major protests at all here. There is a direct correlation between the number of people involved in & informed about our politics and the quality thereof. The last few decades have been dominated by the extremes on both sides because they’re the only ones involved.

Cheney famously said “You know, Paul, Reagan proved deficits don’t matter”. It was the careless, heedless spending of the Reagan and later administrations that built up the wall we find ourselves up against. Deficit spending during good times is criminally negligent. If we had any any level of fiscal responsibility, we would have room on the US credit card to spend some money digging our way out of a hole. Instead we find ourselves barely able to service the interest on the debt we already have. It’s hard to see a way out that doesn’t involve a lot of pain.

What Must be Done

- Fix the credit default swap market.

- Stop trying to fix a problem caused by too much cheap credit with 0% interest rates.

- The American people have to educate themselves about this massive fraud and demand justice, using all available peaceful means.

- Forcibly break up every corporation that is ‘too big to fail’ until there is no such thing.

- House prices will fall below historical mean, that is the iron law of the market. Ill-conceived attempts to rewrite mortgages and prop up housing will fail, and must be stopped.

- Our massive debt burden is unsustainable. We must return to fiscal responsibility, live within our means on a personal and national level, and the existing debt must be defaulted or paid down.

- The ridiculous inefficiencies that are dragging us down must be fixed – our tax code, our health care system, medicare and social security are all unsustainable.

- Term limits for congress. Could anything be more obvious, more broadly supported by the citizens, and yet completely ignored by Washington and the media?

- Campaign finance reform. The bums must be thrown out, and replaced with people who aren’t judged by how good they look on tv, how morally flexible they are, and how much ass they can kiss. The only way this happens is if our elections stop requiring tens of millions to run for office.

- Bring manufacturing back. Depending on rival countries for our every need is a perfect way to guarantee our own decline while we finance other countries’ ascendance.

- End our stupid, pointless, destructive wars. Rome, Britain, Spain… all empires destroyed in part thanks to massive military spending. That’s the road we’re on.

Best Case Scenario

- Massive prosecutions of the fraud that made up many of the mortgages in the last 10 years.

- China or Japan forgives some of our debt out of their own self-interest.

- We end our wars and bring our soldiers home, making us safer and saving us trillions.

- The lies, obfuscation and constant policy changes will end, and investors will have confidence in a transparent system again.

- The administration will pick a plan for the banks & homeowners and stick to it.

- A long period of weak or negative growth as we work off the massive amounts of debt on all levels.

- 14% unemployment at the peak, slowly dropping over time.

- An eventual return to slow & steady growth, and sensible fiscal policies. We begin to pay off our massive debt burden, personally and nationally.

I give this a very small chance of happening.

Worst Case Scenario

- We keep bailing out the banks, refuse to prosecute the guilty, and continue the wealth transfer to the rich.

- Unemployment gets to depression levels.

- We add $2T or more to the deficit every year for 5 or more years, until we have 200% of our GDP in debt.

- China or someone else recovers before we do, and appeals to investors who now demand a higher interest rate on US debt. The fed either hyperinflates by buying all our debt themselves, or all interest rates go up. Refer to the 70s for high interest rate, high inflation, low growth scenarios.

- The world stops using the dollar as the reserve currency, and we are forced to buy oil and such in other currencies. This will turn the inflation gun back into our own faces.

- Civil unrest becomes a major issue as citizens eventually figure out what’s been done to them.

- Massive drops in US GDP -10% or more year over year.

- Basically a re-run of the depression, but now with computers! No one has any idea how this would play out. The world is so interconnected that there’s a good chance that it will be global.

I give this a 20% of happening within the next 10 years.

Most Likely Scenario

- House prices go flat after bottoming out 30% lower from here. They stay roughly flat for 5-10 years as the unsold inventory is worked off.

- Health care reform will hurt that sector of the market, which has previously been pretty strong. This will drive the stock market lower. If reform is done properly, it will save money.

- More and more trillions will be required for various emergencies – natural disasters, pointless endless wars, and bailouts aplenty. China will keep buying our debt for at least the next year or two. Our debt ‘float’ will go from 6T not too long ago to 13 or more. This takes money out of other markets.

- Tent cities and mass homelessness will plague the country, another event the government should have been prepared for but will be ‘surprised’ by, even though there have been news reports about it for over a year.

- Unemployment will get over 10% by the official tally, which is a severe understatement of the true number.

- Social order should be ok for the next couple years, as the true pain is at least that far off (if it comes). Having an adult in charge will go a long ways towards building confidence.

- The Dow Jones will break below 6,000 before the end of 2009, although it will have a violent path. It won’t break through 10k for at least 2 years – probably more like 5.

- Many states are near bankrupt because their budgets reflected massively inflated property values. Tax revenues will be far short of expectations, forcing spending cuts or federal bailouts.

- Recovery – who knows? I have never read a realistic scenario for recovery that didn’t depend on skittle-shitting unicorns dropping money on everyone. It will be a long, hard road.

Recommended Reading

Informative web sites:

- Baseline Scenario

- Calculated Risk

- Cafe American

- Charles Smith

- Market Ticker

- Paul Krugman

- Culture of Life News

Books I can recommend:

- The Black Swan: The Impact of the Highly Improbable

This concept will have a major impact on meta thinking for the rest of human history. The impact of events that are impossible to predict is undeniable, and understanding their impact is crucial. - The Return of Depression Economics and the Crisis of 2008

Krugman explains the causes and fixes for our financial crisis in a clear, understandable way. - Bad Samaritans: The Myth of Free Trade and the Secret History of Capitalism

Chang, who grew up during South Korea’s economic awakening, dispels the myths and hypocrisy of the neo-liberal free trade philosophies designed to ‘kick away the ladder’ for emerging economies. - The New Paradigm for Financial Markets: The Credit Crisis of 2008 and What It Means

Soros expounds on a new theory that is as obvious as it is ignored by current economic theories – that there is a feedback loop in our all-too-human markets that can be self-reinforcing, leading to massive bubbles if uncontrolled. - The World Is Flat 3.0: A Brief History of the Twenty-first Century

Friedman provides an excellent history of how the world became so unavoidably and irrevocably inter-connected, and how to survive in the new paradigm. I haven’t read Hot, Flat, and Crowdedyet, but I’m sure it’s excellent as well.

Disclaimer

I’m not an economist, just an interested reader who has been studying this thing for 2 years. Nothing in this document should be construed as investment advice. Any claims or facts should be verified independently. Copyright David Norris 2009. Feel free to distribute freely.

More from Fourth Wave

The following two tabs change content below.

David Norris

Owner at Fourth Wave ConsultingI have been working with computers and web sites for 20+ years, and have enjoyed mastering many areas of technology. I have been building websites for about 15 years, and working with NetSuite for more than 10. I have worked with dozens of small and medium-sized companies in that time, helping them to understand and leverage the latest tools to grow their business. My business is all about helping you to maximize your business, and I prefer to establish long-term relationships with clients who are dedicated to embracing smart ways to optimize and expand their business.Latest posts by David Norris (see all)

- NetSuite Announces Plans to End Promotion Functionality for Site Builder - January 16, 2020

- Most NetSuite Websites Are No Longer Tracking Safari Conversions for Adwords - November 20, 2017

- Make Your NetSuite Site Builder Site Secure – HTTPS Throughout - May 28, 2017

- An Introduction to Automating XML Sitemaps for NetSuite Companies - November 13, 2016

- An Introduction to NetSuite’s Reference Checkout & My Account Bundles - April 18, 2016